COST ALERT: California’s average minimum coverage premium of $841/year is 12% above the $750 national average for liability-only policies.

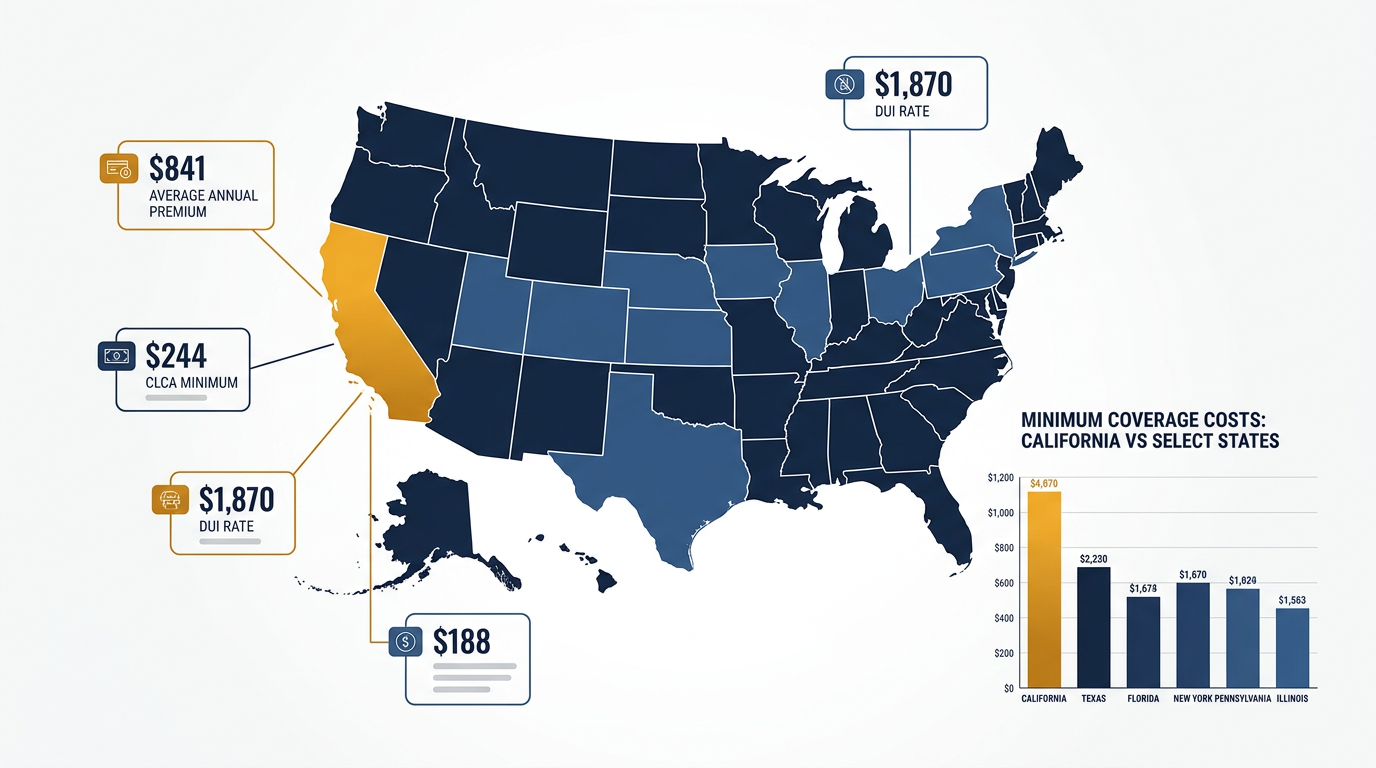

California’s minimum car insurance requirement comes with an average annual premium of $841 for the legally mandated coverage — roughly 12% higher than the national average of $750 per year for comparable liability-only policies. Understanding exactly what the state requires, and what that coverage actually costs you, is the first step toward making a smart purchasing decision.

What California’s Minimum Coverage Requirements Actually Are

California operates under a 15/30/5 liability framework. That means every driver must carry at least $15,000 in bodily injury liability per person, $30,000 in bodily injury liability per accident, and $5,000 in property damage liability. These are among the lowest minimums of any U.S. state, yet California’s dense population, high repair costs, and elevated medical expenses push average premiums well above what those modest limits might suggest. The state does not require uninsured motorist coverage, collision, or comprehensive insurance — though adding those components brings the average annual premium to approximately $2,190 statewide.

Why California’s Minimum Coverage Costs What It Does

Several structural factors explain why Californians pay $841 per year on average just for the legal minimum. First, California prohibits insurers from using credit scores as a rating factor — a consumer-friendly rule that simultaneously compresses the discount pool and pushes base rates upward for everyone. Second, the state’s repair costs run approximately 18% above the national median, with the average auto repair claim reaching $4,200 compared to roughly $3,560 nationally. Third, traffic density in metro corridors like Los Angeles, the Bay Area, and San Diego generates claim frequency that filters directly into premium pricing. Los Angeles County drivers pay an average of $1,104 per year for minimum coverage alone — 31% more than the statewide average. Rural counties like Shasta or Siskiyou, by contrast, can see minimum-coverage premiums closer to $620 annually.

Cheapest Options for California Minimum Coverage

Among the most competitively priced options available in the California market, minimum-coverage annual premiums vary significantly by carrier. The lowest documented average rates for a 35-year-old driver with a clean record hover around $450–$520 per year from budget-oriented carriers, while mid-tier carriers average closer to $700–$780 annually. Premium carriers with strong service ratings average $920 or more per year for the same legal minimum. Note that California also operates the Low Cost Auto Insurance Program (CLCA), a state-sponsored plan designed for income-eligible drivers, offering minimum coverage for as little as $244 per year for qualifying applicants — making it one of the most significant cost-reduction tools available to California residents who meet the income thresholds.

How to Reduce Your Minimum Coverage Premium

The single most impactful action a California driver can take is maintaining a clean driving record. A single at-fault accident raises the average minimum-coverage premium by approximately $340 per year in California — a 40% increase on the $841 baseline. A DUI conviction can spike that figure to an average of $1,870 per year, more than doubling the standard rate. Beyond record maintenance, bundling auto with renters or homeowners insurance typically saves California drivers between $80 and $160 annually depending on the carrier. Installing a telematics or usage-based device can yield discounts of up to 20%, translating to roughly $168 off the statewide average premium. Paying your full annual premium upfront instead of monthly can save an additional $50–$90 per year, as monthly installment fees in California average $6–$8 per payment.

What Affects Your Individual Rate

California law restricts which factors insurers can use, but the permitted variables still create wide premium variation. Your ZIP code is arguably the single biggest driver — moving from rural Fresno County (average $590/year) to central Los Angeles (average $1,180/year) can nearly double your minimum-coverage cost without any change to your driving behavior. Age plays a major role: teenage drivers in California pay an average of $1,640 per year for minimum coverage, while drivers aged 35–55 see the lowest rates, averaging $760–$810 annually. Seniors aged 75 and older see premiums climb back toward $990 per year on average. Your vehicle matters too — a newer vehicle with a higher replacement value doesn’t change your liability premium directly, but registration data ties into risk profiling. Finally, your annual mileage factors in: driving fewer than 7,500 miles per year can reduce your premium by an average of $95–$130 annually compared to a driver logging 15,000 miles.

The Bottom Line on California Minimum Requirements

The $841 annual average for California’s 15/30/5 minimum coverage is a starting point, not a destination. Those limits — particularly the $5,000 property damage floor — are dangerously low in a state where the average new vehicle costs over $48,000. A single fender-bender in a parking lot can exceed that $5,000 threshold, leaving you personally liable for the remainder. Most insurance professionals recommend upgrading to at least 50/100/50 limits, which brings the California average premium to approximately $1,050 per year — a $209 annual increase that buys substantially more financial protection. Shopping the market every 12 months and using California’s robust competitive landscape remains your best tool for keeping costs manageable while maintaining adequate protection.

| State | Avg Annual Premium (Min Coverage) | vs National Avg | Cheapest Provider Category | Most Expensive Category | Key Rating Factor |

|---|---|---|---|---|---|

| California | $841 | +12% | Budget carriers (~$480/yr) | Premium carriers (~$940/yr) | ZIP code / metro density |

| Texas | $772 | +3% | Budget carriers (~$430/yr) | Premium carriers (~$890/yr) | Weather/hail claims |

| Florida | $1,060 | +41% | Budget carriers (~$610/yr) | Premium carriers (~$1,200/yr) | No-fault fraud costs |

| New York | $998 | +33% | Budget carriers (~$570/yr) | Premium carriers (~$1,150/yr) | Urban density/litigation |

| Ohio | $420 | -44% | Budget carriers (~$240/yr) | Premium carriers (~$510/yr) | Low litigation rates |

| Michigan | $1,180 | +57% | Budget carriers (~$720/yr) | Premium carriers (~$1,400/yr) | Unlimited PIP mandate |

| Arizona | $710 | -5% | Budget carriers (~$390/yr) | Premium carriers (~$820/yr) | Uninsured driver rate |

Frequently Asked Questions

What is the minimum car insurance required in California?

California requires 15/30/5 liability coverage: $15,000 per person, $30,000 per accident in bodily injury, and $5,000 in property damage liability.

How much does California minimum car insurance cost per year?

The average annual cost of California minimum car insurance is $841, which is approximately 12% higher than the national average of $750 per year.

What is the cheapest way to get minimum coverage in California?

Income-eligible drivers can access the state’s Low Cost Auto Insurance Program (CLCA) for as little as $244 per year, while standard budget carriers average around $480 annually.

How much does a DUI raise car insurance in California?

A DUI conviction raises the average California minimum-coverage premium to approximately $1,870 per year, more than double the standard $841 statewide average.

COST ALERT: California’s average minimum coverage premium of $841/year is 12% above the $750 national average for liability-only policies.

California’s minimum car insurance requirement comes with an average annual premium of $841 for the legally mandated coverage — roughly 12% higher than the national average of $750 per year for comparable liability-only policies. Understanding exactly what the state requires, and what that coverage actually costs you, is the first step toward making a smart purchasing decision.

What California’s Minimum Coverage Requirements Actually Are

California operates under a 15/30/5 liability framework. That means every driver must carry at least $15,000 in bodily injury liability per person, $30,000 in bodily injury liability per accident, and $5,000 in property damage liability. These are among the lowest minimums of any U.S. state, yet California’s dense population, high repair costs, and elevated medical expenses push average premiums well above what those modest limits might suggest. The state does not require uninsured motorist coverage, collision, or comprehensive insurance — though adding those components brings the average annual premium to approximately $2,190 statewide.

Why California’s Minimum Coverage Costs What It Does

Several structural factors explain why Californians pay $841 per year on average just for the legal minimum. First, California prohibits insurers from using credit scores as a rating factor — a consumer-friendly rule that simultaneously compresses the discount pool and pushes base rates upward for everyone. Second, the state’s repair costs run approximately 18% above the national median, with the average auto repair claim reaching $4,200 compared to roughly $3,560 nationally. Third, traffic density in metro corridors like Los Angeles, the Bay Area, and San Diego generates claim frequency that filters directly into premium pricing. Los Angeles County drivers pay an average of $1,104 per year for minimum coverage alone — 31% more than the statewide average. Rural counties like Shasta or Siskiyou, by contrast, can see minimum-coverage premiums closer to $620 annually.

Cheapest Options for California Minimum Coverage

Among the most competitively priced options available in the California market, minimum-coverage annual premiums vary significantly by carrier. The lowest documented average rates for a 35-year-old driver with a clean record hover around $450–$520 per year from budget-oriented carriers, while mid-tier carriers average closer to $700–$780 annually. Premium carriers with strong service ratings average $920 or more per year for the same legal minimum. Note that California also operates the Low Cost Auto Insurance Program (CLCA), a state-sponsored plan designed for income-eligible drivers, offering minimum coverage for as little as $244 per year for qualifying applicants — making it one of the most significant cost-reduction tools available to California residents who meet the income thresholds.

How to Reduce Your Minimum Coverage Premium

The single most impactful action a California driver can take is maintaining a clean driving record. A single at-fault accident raises the average minimum-coverage premium by approximately $340 per year in California — a 40% increase on the $841 baseline. A DUI conviction can spike that figure to an average of $1,870 per year, more than doubling the standard rate. Beyond record maintenance, bundling auto with renters or homeowners insurance typically saves California drivers between $80 and $160 annually depending on the carrier. Installing a telematics or usage-based device can yield discounts of up to 20%, translating to roughly $168 off the statewide average premium. Paying your full annual premium upfront instead of monthly can save an additional $50–$90 per year, as monthly installment fees in California average $6–$8 per payment.

What Affects Your Individual Rate

California law restricts which factors insurers can use, but the permitted variables still create wide premium variation. Your ZIP code is arguably the single biggest driver — moving from rural Fresno County (average $590/year) to central Los Angeles (average $1,180/year) can nearly double your minimum-coverage cost without any change to your driving behavior. Age plays a major role: teenage drivers in California pay an average of $1,640 per year for minimum coverage, while drivers aged 35–55 see the lowest rates, averaging $760–$810 annually. Seniors aged 75 and older see premiums climb back toward $990 per year on average. Your vehicle matters too — a newer vehicle with a higher replacement value doesn’t change your liability premium directly, but registration data ties into risk profiling. Finally, your annual mileage factors in: driving fewer than 7,500 miles per year can reduce your premium by an average of $95–$130 annually compared to a driver logging 15,000 miles.

The Bottom Line on California Minimum Requirements

The $841 annual average for California’s 15/30/5 minimum coverage is a starting point, not a destination. Those limits — particularly the $5,000 property damage floor — are dangerously low in a state where the average new vehicle costs over $48,000. A single fender-bender in a parking lot can exceed that $5,000 threshold, leaving you personally liable for the remainder. Most insurance professionals recommend upgrading to at least 50/100/50 limits, which brings the California average premium to approximately $1,050 per year — a $209 annual increase that buys substantially more financial protection. Shopping the market every 12 months and using California’s robust competitive landscape remains your best tool for keeping costs manageable while maintaining adequate protection.

| State | Avg Annual Premium (Min Coverage) | vs National Avg | Cheapest Provider Category | Most Expensive Category | Key Rating Factor |

|---|---|---|---|---|---|

| California | $841 | +12% | Budget carriers (~$480/yr) | Premium carriers (~$940/yr) | ZIP code / metro density |

| Texas | $772 | +3% | Budget carriers (~$430/yr) | Premium carriers (~$890/yr) | Weather/hail claims |

| Florida | $1,060 | +41% | Budget carriers (~$610/yr) | Premium carriers (~$1,200/yr) | No-fault fraud costs |

| New York | $998 | +33% | Budget carriers (~$570/yr) | Premium carriers (~$1,150/yr) | Urban density/litigation |

| Ohio | $420 | -44% | Budget carriers (~$240/yr) | Premium carriers (~$510/yr) | Low litigation rates |

| Michigan | $1,180 | +57% | Budget carriers (~$720/yr) | Premium carriers (~$1,400/yr) | Unlimited PIP mandate |

| Arizona | $710 | -5% | Budget carriers (~$390/yr) | Premium carriers (~$820/yr) | Uninsured driver rate |

Frequently Asked Questions

What is the minimum car insurance required in California?

California requires 15/30/5 liability coverage: $15,000 per person, $30,000 per accident in bodily injury, and $5,000 in property damage liability.

How much does California minimum car insurance cost per year?

The average annual cost of California minimum car insurance is $841, which is approximately 12% higher than the national average of $750 per year.

What is the cheapest way to get minimum coverage in California?

Income-eligible drivers can access the state’s Low Cost Auto Insurance Program (CLCA) for as little as $244 per year, while standard budget carriers average around $480 annually.

How much does a DUI raise car insurance in California?

A DUI conviction raises the average California minimum-coverage premium to approximately $1,870 per year, more than double the standard $841 statewide average.

Leave a Reply